Retirees who primarily rely on their living annuity investments to provide them with a steady stream of income are often haunted by the question: How do I make my income last throughout retirement? Shaun Duddy discusses four golden rules that, if applied appropriately, can help make your retirement savings last.

There are four rules that are essential long-term drivers of success for living annuity investors. Below I will elaborate on them.

Rule 1: Plan for a reasonable number of years in retirement

Planning for a long retirement is very important to sustaining your income. The risk of running out of money in retirement can be reduced with proper planning. The number of years you need to plan for essentially comes down to how certain you want to be that you have planned for enough.

To give yourself a 90% chance that you have planned for enough years and will not outlive your planning horizon, research suggests that living annuitants should plan for approximately 40 years at age 55, through to 10 to 15 years at age 85.

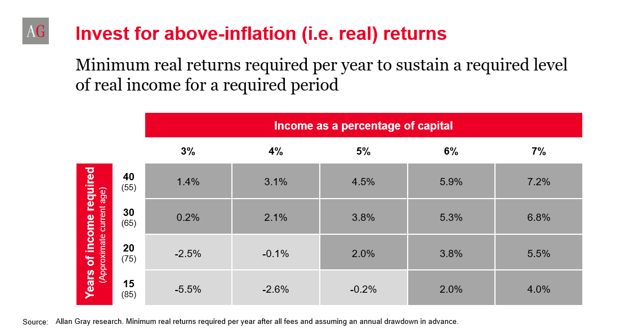

Rule 2: Invest for above-inflation (i.e. real) returns

Whenever you invest, you are looking to get the best possible returns, while accounting for the risk you are able to tolerate. For a living annuitant this is even more important because you need to understand what level of real returns are required to sustain your required level of income for the duration of your retirement.

To illustrate this, let’s consider the table below: An investor who is drawing 4% of their capital and wants to increase it by inflation each year, and is planning for a 30-year retirement, would require real returns of 2.1% per year in each of the 30 years (i.e. with no volatility), as shown in the table below. In this scenario, if inflation is 6.1% per year, then you would need a return of about 8.2% per year in each of the 30 years. These numbers are even higher once you add in volatility.

However, this picture changes significantly if you increase the drawdown rate and/or the number of years in retirement.

So how do you go about investing the money in a living annuity to maximise the chances of making your income last? First and foremost, you need to ensure that you have an appropriate exposure to growth assets. Long-term data shows that growth assets like equities are essential for real returns. You would need a minimum of 50% exposure to growth assets and, depending on your risk tolerance, there has been value in going up to 60 – 70%.

Rule 3: Manage volatility but not at the expense of real returns

In addition, research shows that being able to reduce volatility without (significantly) reducing real returns or being able to increase real returns without (significantly) increasing volatility, increases the probability of success in a living annuity. Research further demonstrates that adding an appropriate level of offshore exposure has been a good way to do this but be cautious against diving in headfirst.

It has been most appropriate to have at least 50% exposure to growth assets, and then to manage volatility through an appropriate amount of offshore diversification, historically in the region of 30 – 50%, and through good quality active management.

Rule 4: Draw a reasonable level of income

With 30 years of income required, starting drawdowns in the region of 4% to 4.5% and below have had probabilities of success in the region of 90% and above, assuming adherence to rules 1 - 3. Beyond this range of drawdowns, the probabilities of success start to decrease.

But what if you need to draw down a higher level of income? What are your options?

In this case, there are two options available: Take income increases below inflation i.e., start with a higher level of income but take lower increases to offset this over your retirement, or consider transferring some or all of your risk to an insurer with a guaranteed annuity.

A guaranteed annuity offers annuitants a guaranteed income for life, regardless of how long their retirement is, and it typically offers a higher level of starting income than what may be considered sustainable in a living annuity. These benefits come at the cost of reduced flexibility and lower or no capital legacy on death.